SMM April 24 News:

Price Review:

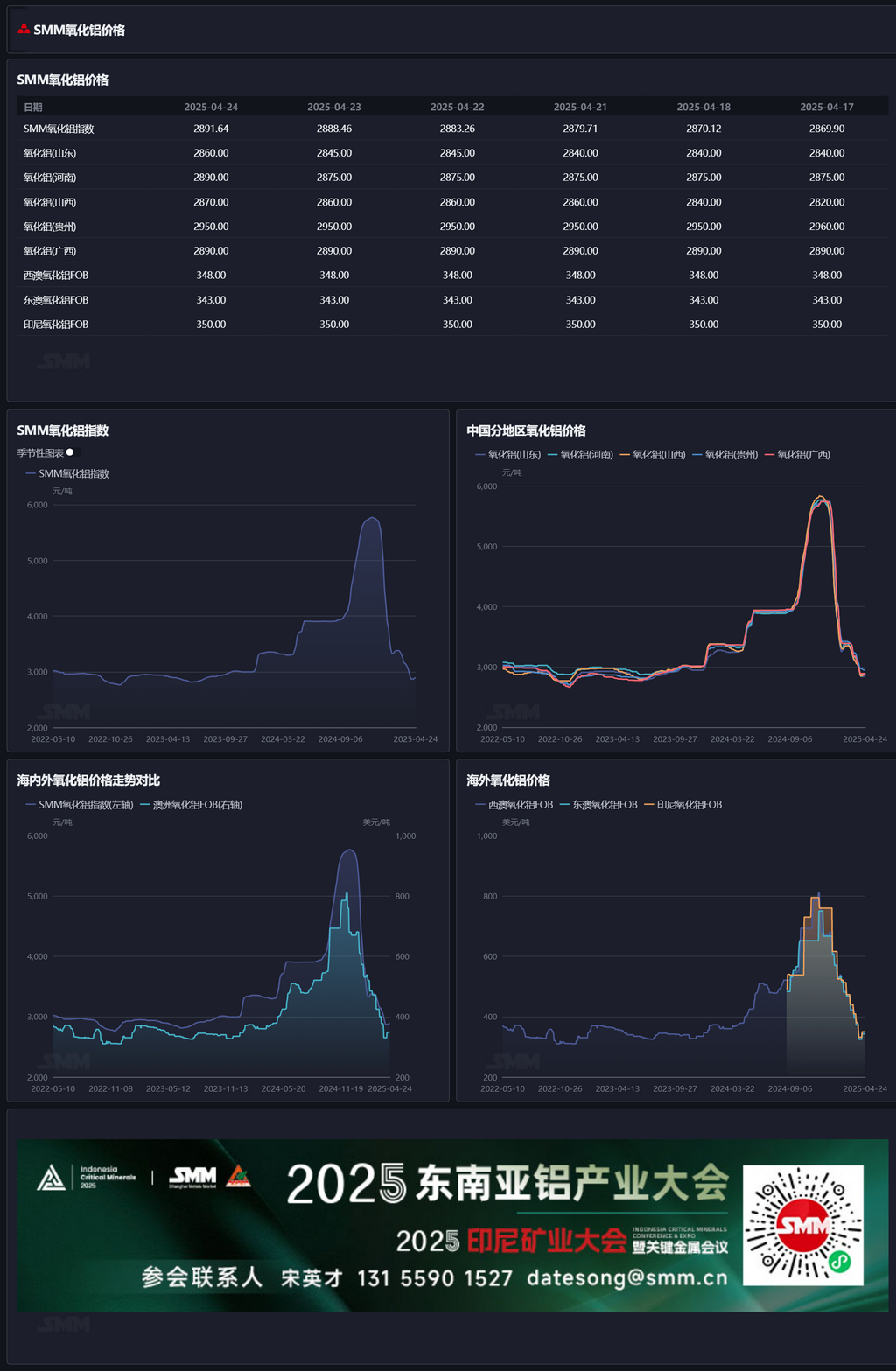

As of this Thursday, the SMM regional weighted index stood at 2,891.64 yuan/mt, up 21.74 yuan/mt WoW. Shandong reported 2,840-2,880 yuan/mt, up 20 yuan/mt WoW; Henan reported 2,860-2,920 yuan/mt, up 15 yuan/mt WoW; Shanxi reported 2,870-2,910 yuan/mt, up 30 yuan/mt WoW; Guangxi reported 2,860-2,920 yuan/mt, flat WoW; Guizhou reported 2,930-2,970 yuan/mt, down 10 yuan/mt WoW; Bayuquan reported 3,110-3,190 yuan/mt.

Overseas Market:

As of April 24, 2025, the FOB Western Australia alumina price was $348/mt, with an ocean freight rate of $20.50/mt. The USD/CNY exchange rate selling price was around 7.32, translating to a domestic mainstream port selling price of approximately 3,126 yuan/mt, 234 yuan/mt higher than domestic alumina prices, keeping the alumina import window closed. This week, one new overseas alumina spot transaction was recorded, with the transaction price flat compared to the previous one: on April 17, 20,000 mt of overseas alumina was traded at $347.5/mt FOB Western Australia, with a May shipment schedule.

Domestic Market:

According to SMM data, as of this Thursday, the national metallurgical-grade alumina existing capacity totaled 107.62 million mt/year, with operating capacity at 83.62 million mt/year. Weekly production was 1.604 million mt, and the national alumina operating rate decreased 1.22 percentage points WoW to 77.70%, mainly due to some new alumina capacity entering the commissioning phase, increasing existing capacity. The weekly operating capacity rebounded 740,000 mt/year WoW, primarily because some alumina capacity completed maintenance and resumed production. Shandong's alumina operating rate remained at 91.74% WoW; Shanxi's alumina operating rate decreased 1.2 percentage points WoW to 70.40%; Henan's alumina operating rate decreased 4.58 percentage points WoW to 55.83%; Guangxi's alumina operating rate decreased 5.37 percentage points WoW to 88.64%.

During the period, sporadic transactions occurred in the alumina spot market, with overall transaction prices stabilizing. Alumina prices in north China rebounded slightly. By region: Xinjiang aluminum plants tendered and procured some alumina, with delivery-to-factory prices around 3,190 yuan/mt; Shandong accumulated 4,000 mt of alumina transactions, with transaction prices at 2,865-2,870 yuan/mt; Shanxi recorded 5,000 mt of alumina transactions, with transaction prices at 2,890 yuan/mt; Henan recorded 2,000 mt of alumina transactions, with transaction prices at 2,920 yuan/mt; Guizhou accumulated 5,000 mt of alumina transactions, with ex-factory prices at 2,945-2,950 yuan/mt.

Overall:

This week, some alumina refineries completed maintenance and resumed production; meanwhile, new maintenance and production cut news emerged, with alumina operating capacity both increasing and decreasing. Overall, weekly operating capacity rebounded slightly. As of this Thursday, according to SMM statistics, national alumina operating capacity was 83.62 million mt/year, up 740,000 mt/year WoW. Due to concentrated maintenance and production cuts, alumina operating capacity has been below the theoretical demand for aluminum production for several consecutive weeks, tightening alumina spot supply. As a result, alumina spot prices stabilized, with slight rebounds in north China. Subsequent tracking of alumina maintenance capacity resumption progress, new capacity commissioning progress, and new maintenance and production cut news is needed. Short-term prices are expected to fluctuate.